Internet Capital Markets: A Problem Half Solved

This piece was originally published as an X Article on March 1, 2026. You can find the original here.

There’s a lot of experimentation going on with internet capital markets. You can trade a wide spectrum of assets, onchain, 24/7. You can raise capital, onchain, 24/7. You can build communities, onchain, 24/7. Tokens lie at the heart of this, but more so, its high quality teams and founders that make this happen. Everything boils down to how good the team is and how bad they want it. But still, tokens are broken. We know this. Not all tokens, but most.

I wanted to share a few thoughts I had about MetaDAO and the design space they are solving problems within; permissionless capital formation. It currently solves for unruggability in a space that will soon define rugs as crimes.

Tokens Do Not Have Enforceable Rights

The upside volatility or reflexivity on tokens has covered over serious cracks in the way they are launched, valued, or treated. The bottom line is that for most tokens, there’s no real rights for token holders, and as a result, there is no difference between most tokens and memecoins (also tokens). This has actually found its way to mainstream relevance quite often within crypto in the last few months as we’ve seen two or three large scale acquisitions, where the companies had live tokens but the acquirers sidestepped them by “acquiring the team” or acquiring the “labs entity” behind the tokens, leaving tokenholders with nothing. The framing was something like this:

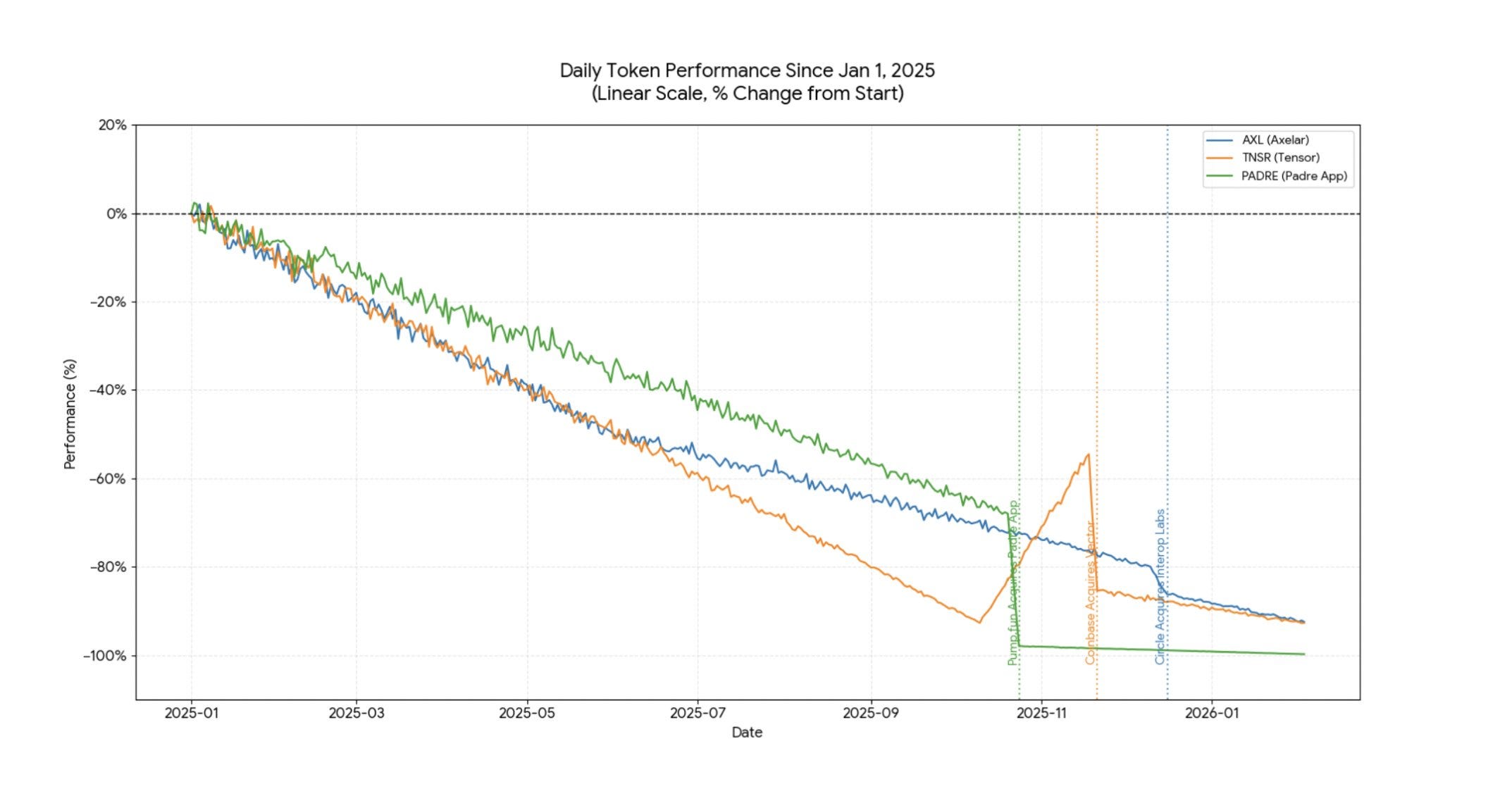

AXLR tokenholders got nothing when acquired by Circle

TNSR tokenholders got nothing when Coinbase acquired Vector

(which the team had initially mentioned was backed by the TNSR token)

PADRE tokenholders got nothing when Pump Fun acquired Padre App

It was rather clear that the token was simply a perceived reflection of value rather than real value, and all the acquiring entities involved (Coinbase, Pump, Circle) likely pursued the acquisitions in the way that they did, given that there was no explicit clarity on tokenholder rights, and hence, they were able to pay substantially less vs what they would have had to had there been explicit rights. If there were explicit rights for tokens and tokenholders, the acquirers would not have even wanted to go the sidestep route, and tokenholders would have got a share in the benefits of the acquisition.

That being said, I think this is a regulatory and investor protection problem. Reasoning from first principles, in the absence of clear regulation around tokens and their rights and protections, there was a clear incentive to operate in a gray area. This has been an open secret in crypto since the Ethereum ICO. Once we have clear regulation in place, this problem is more than half solved.

While MetaDAO has a liquid token, META - the product is still in its experimentation phase. Futarchy has been around since the 2000s, but no real market applications have emerged since, until crypto. It makes sense that the mechanism has been able to catch on with crypto markets, just given the total number of outright scams/fraud we have seen in the space. Heightened awareness about futarchy and smart contract enforced rights in a space full of rugs was always a likely outcome.

The design space for experimentation is quite wide, which makes this investment angle interesting, however, there is real adoption risk of futarchy. MetaDAO has iterated on their product multiple times in their 24 months of operation, and at their core, it is now a launchpad token product (an ICO product) that applies onchain tokenholder protections to the tokens that they help launch, while also helping bridge the gap with real world legal enforcement. They provide guarantees for investors, and by doing so, aim to unlock latent capital for founders.

I think the bet here isn’t an explicit bet on futarchy, but a bet on the idea that permissionless capital raises in a controlled environment will lead to large venture outcomes. The bet is also on the fact that the two founders, Metaprophet and Kollan House will do whatever it takes to try to realise this ambitious vision. With this in mind, despite the fact that they have a liquid token (META) that is currently trading at a $95M FDV (liquidity is rather thin), I believe the correct way to approach this investment, both in size and intent, would be as a venture investment.

Thinking About Venture Investing From First Principles - Betting on High Velocity Founders

MetaDAO is now essentially solving for investor protected, global, and permissionless capital formation. It allows people around the world to raise money based on programmatic guarantees, but also, it allows investors to participate in early stage deals permissionlessly without any risk of getting outright rugged. It makes sense to think about what kind of profile of projects Metadao enables and the second order effects of this model.

Thinking about venture investing from first principles, it is a bet on both an idea and the founding team. You bet on their ability to innovate, execute and hire well. Ideally, as a venture investor you want access to the best founders working on difficult problems or big problems. The honest truth is that these types of founders may not necessarily struggle to raise capital. MetaDAO appeals to a founder base that struggles to raise private capital, either as a result of geography (no access to top tier capital), or simply because top tier capital (or even second tier capital) wasn’t interested in the idea. While crypto is the perfect platform by which to raise capital, it doesn’t inherently solve for the quality of founders. And in its nascent stage, neither does MetaDAO. Ideally, you want to provide a platform for high quality founders to raise capital, and you want to give retail investors access to these founders. Echo tried to do this before it got acquired by Coinbase and proved rather successful. (valued at ~$400M). Echo’s value lay in the fact that it gave retail access to high quality dealflow, and not explicitly, unruggable dealflow.

Going one more layer deep, MetaDAO’s model removes the need for trusting that a founder knows what the best use of capital is, and enforces conditions for use of any capital raised. Nothing happens without the tokenholders saying so. The whole point of running a startup from scratch is that the founder claims complete agency over end to end execution. I think the best founders and teams would rather have a pool of aligned, strategic investors and the will to deploy and use the capital to grow their business as they see fit, than be beholden to a set of anonymous participants (although some may be aligned). By and large, it is hard for anyone adjacent to a founder to understand the direction they want to take the company in, and it should be their decision, and theirs alone. And for better or for worse, it is this set of decisions that lead to large outcomes. I would tend to believe that the current structure of MetaDAO likely even repels elite founders who need freedom to do their best work. It most definitely deters bad actors, as they can’t outright rug. But the fact that this model could deter the best founders, is problematic.

You can make the argument that MetaDAO’s model unlocks dark talent - talent that has no goodwill but is well intentioned, and couldn’t raise capital any other way. This is powerful, however, it will take a lot of time to scale, and eventually, you need the founders to execute and deliver large outcomes. But one large outcome is all it takes.

I think in its current form, while filtering out bad actors, the MetaDAO model also tends to filter out excellent founders and leaves behind a pool of average founders who explicitly cannot rug. As a venture investor, the whole point is to be willing to take the risk of betting on a top tier founder without any programmatic guarantees of how they can operate than on an average team that cannot rug the token. However, this can change with one launch - and that is the reason I think MetaDAO remains interesting.

I think it becomes clear that the bet on MetaDAO now is on discovery. Dark talent + permissionless capital formation is a very powerful combination, and MetaDAO is well positioned to enable and benefit from this. The founders have shown a deep rooted willingness to solve this problem, while also staying flexible and pivoting their product to stay relevant.